Blockwall - April 2026 - What happened in Web3?

Dear Founders, Investors, and Friends,

It’s great to welcome you back to the April 2026 edition of Blockwall Insights. We apologize for the slight delay in getting this to you. The past few weeks have been packed with a full calendar, but we are glad to finally have it in your hands. Here’s what we’re covering today:

Prediction Markets, Hyperliquid’s HIP-4, and Rothera

RWA Perpetuals Prove Their Worth on Weekends

KfW’s Third Digital Bond Moves Tokenized Debt Beyond the Pilot Phase

Blockwall Portfolio Update

Key Events of the Last Few Weeks

What We’ve Been Reading

Executive Summary

April showed how quickly crypto market structure is moving from isolated use cases toward integrated financial infrastructure.

Prediction markets were one of the clearest signals. Volumes on platforms such as Polymarket and Kalshi continued to scale, while Robinhood prepared the Q2 launch of Rothera, its joint venture with Susquehanna. By acquiring a CFTC-licensed exchange and clearinghouse, Rothera gives Robinhood the ability to vertically integrate prediction markets, controlling distribution, liquidity, product selection and economics rather than relying on third-party venues.

At the same time, Hyperliquid demonstrated what always-on execution can mean in practice. During periods when legacy commodity markets were closed, oil-linked perpetuals on Hyperliquid absorbed significant trading volume and, according to TD Securities, priced in roughly 80% of the subsequent WTI move before CME reopened. This matters because it shows that onchain markets are no longer only alternative venues; in moments of market stress, they can become the first place where new information is reflected. HIP-4 extends this logic from real-world asset perpetuals to binary outcome markets, pointing toward a unified execution layer for financial and information markets.

In Europe, KfW’s third digital bond marks another step in tokenization’s institutional maturation. Rather than simply proving that a regulated bond can be issued onchain, the transaction is designed to test resilience under live conditions, including a change of registrar and migration from Polygon to the bank-backed RL1 network while the bond remains outstanding.

These developments converge on a single insight: continuous, regulated onchain markets are moving from theory to live market structure.

Prediction Markets, Hyperliquid’s HIP-4, and Rothera: The Convergence of Information Markets and Execution Layers

Prediction markets emerged as one of the clearest signals of crypto’s institutional maturation in April 2026. Volumes surged into the billions as Polymarket and Kalshi captured mainstream attention, while traditional brokerages accelerated their positioning.

On its Q1 2026 earnings call and subsequent investor conferences, Robinhood highlighted preparations for the Q2 launch of Rothera, its joint venture with Susquehanna International Group. Through Rothera’s acquisition of the CFTC-licensed MIAXdx exchange and clearinghouse, Robinhood is building its own regulated prediction market infrastructure. Robinhood serves as the controlling partner and distribution platform, while Susquehanna provides day-one liquidity. Management has stated that the strategy is to vertically integrate prediction markets, giving Robinhood greater control over product development, market economics, and contract listings while reducing reliance on third-party exchanges such as Kalshi. After processing a record 8.8 billion event contracts in Q1, this move positions Robinhood to capture significantly more of the economics internally.

In the decentralized domain, the high-performance perpetuals exchange Hyperliquid made a decisive move to capture this demand by testing HIP-4 (Hyper Improvement Plan) at the end of April. HIP-4 introduces fully collateralized binary outcome contracts directly into the HyperCore execution layer. There is no leverage and no liquidation risk. Traders can seamlessly cross-margin prediction positions with spot and perpetual positions in a single account. By embedding event probabilities into its core engine, Hyperliquid is clearly positioning itself as a unified execution layer for all financial markets.

RWA Perpetuals Prove Their Worth on Weekends

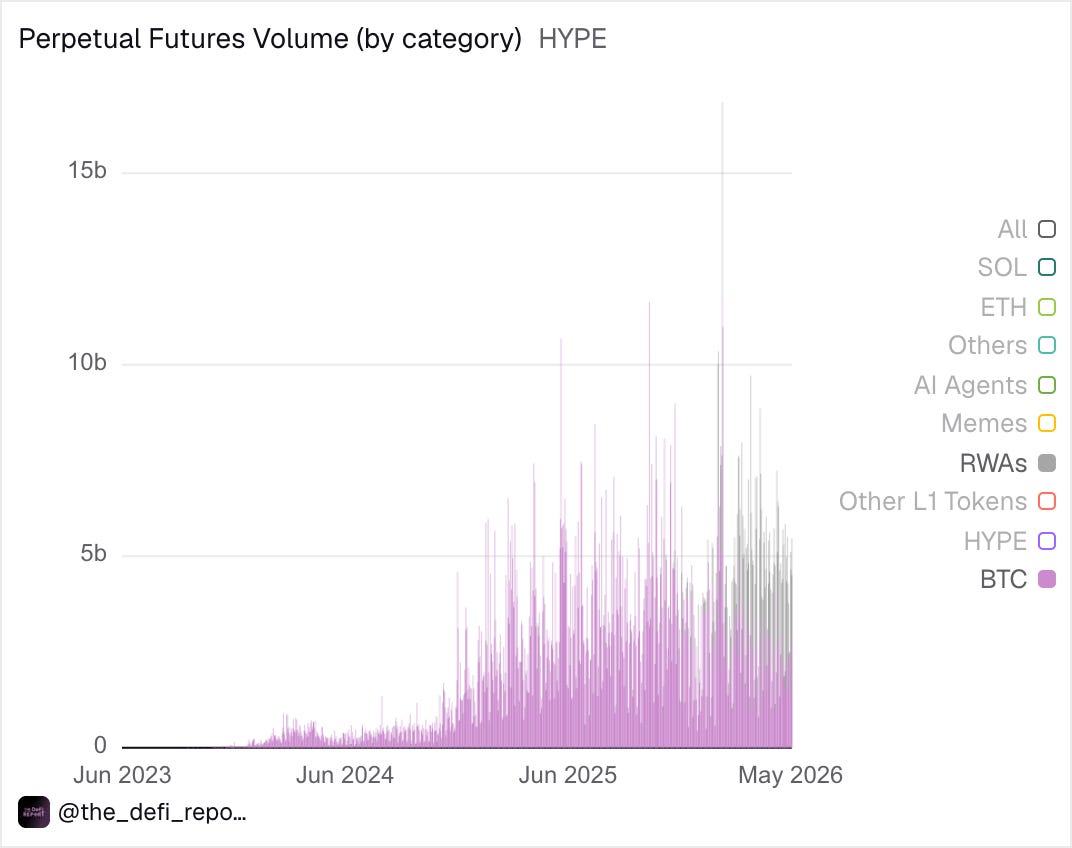

The structural weakness of legacy market hours was on display repeatedly through Q1 and into April, as the U.S.–Israel–Iran conflict and the threat to close the Strait of Hormuz kept crude violently bid. Each time news broke while CME and ICE were dark, overnight and most starkly over weekends, crypto absorbed the flow. Oil-linked perpetuals on Hyperliquid, deployed under HIP-3 by builders such as trade.xyz, became the venue where that risk was priced first. Across the early weekend windows, notional volume scaled from roughly $25 million in the first session to over $550 million within three weekends. On April 8, as ceasefire headlines sent crude reversing, combined WTI and Brent perps cleared north of $3 billion in 24 hours (see Perpetual Futures Volume: by category “RWA”), briefly overtaking Bitcoin as the most-traded market on the platform.

The more important signal was not the volume itself, but where the market price was formed. TD Securities estimated that Hyperliquid had already priced in roughly 80% of the subsequent WTI move before CME reopened. In other words, during a period when traditional commodity markets were closed, the onchain market became the first venue to reflect the new information. This is what a unified execution layer looks like in practice rather than in theory: when an always-on settlement engine is the only venue open during a macro shock, it stops being an alternative and becomes the reference. It is the same architecture HIP-4 extends to event outcomes, and the infrastructure layer we are watching most closely.

Our view

Those two threads run through this month, and they converge on one conclusion. The first is that the demand is no longer hypothetical: prediction-market volumes are compounding, and the weekend oil tape showed that continuous, onchain RWA markets can absorb billions in a single session the moment legacy venues go dark. The second is quieter, but it matters more. The venue that captured that oil volume, trade.xyz, the dominant HIP-3 deployer, holds its position only by committing tens of millions of dollars of its own capital as the required deployment bond. That confines it to the handful of assets liquid enough to justify that risk: oil, major indices and the top metals. The same capital barrier that lets one player own the short tail is exactly what keeps the long tail, emerging-market FX, soft commodities, pre-IPO names, compute, and the new HIP-4 outcome markets, from ever launching. That is a supply constraint, not a demand one. In our view, the more durable opportunity is therefore unlikely to sit with any single market deployer, however dominant, but with the infrastructure that can remove this constraint and expand the universe of markets that can come onchain. That is where we are spending our time, and where we expect our next conviction to be expressed.

KfW’s Third Digital Bond Moves Tokenized Debt Beyond the Pilot Phase

Some of the most consequential infrastructure work in tokenization this year is happening inside the regulated core of European finance. After issuing its first blockchain-based digital bond under the German Electronic Securities Act (eWpG) in July 2024, Germany’s state-owned development bank KfW, among Europe’s largest bond issuers, is now preparing its third digital bond under the same framework in June 2026. Unlike its two predecessors, this one is engineered not to prove again that the technology works, but to stress-test the surrounding infrastructure under live, mid-lifecycle conditions: for the first time, both the register and the blockchain beneath a live tokenized bond will be changed while it is still outstanding.

The bond will be issued on the public Polygon network with the Frankfurt fintech Cashlink as registrar, and then, while the instrument is still live, put through a deliberate dual migration: the registrar role moves from Cashlink to DekaBank, and the bond itself is transferred from Polygon to the European bank-backed, permissioned Regulated Layer One (RL1) via a coordinated cross-ledger migration. On the settlement side, the cash leg links the Bundesbank’s Trigger Solution at issuance with the Eurosystem’s forthcoming Pontes platform for later lifecycle and redemption events. The point of introducing this operational friction is precisely that it is friction: a pivot away from isolated, fair-weather pilots toward the resilient, portable, recoverable infrastructure that institutional scale actually requires.

This reframes the maturity question. Earlier pilots settled whether a regulated security can live on distributed-ledger infrastructure; it can. The open questions are about resilience: whether a live bond survives a change of registrar (no tokenized bond has yet moved between any of Germany’s seven licensed registrars) or a change of chain, and whether payment keeps clearing across systems. KfW frames it as the shift from proving the technology in isolated deals to testing how it holds “beyond fair-weather conditions” and, more deeply, as the difference between digitizing today’s process and digitalizing it: re-engineering the workflow and eventually embedding programmable logic into the instrument or the cash itself.

This was the central theme at our Blockwall Investor Summit 2025, where Bert Staufenbiel of KfW and Christoph Hock of Union Investment discussed the shift from simply digitizing existing instruments to genuinely redesigning the processes around them (panel: “Institutional Ready: Web3 goes Mainstream”). The throughline was that tokenization is moving from experiment to expected market practice on the buy-side, and that modernizing away from siloed legacy systems has become a matter of European competitiveness and digital sovereignty rather than a discretionary technology project.

Blockwall Portfolio Update

AI agents are only as useful as the data they can reach and the compliance guarantees behind them, and in regulated industries both are genuinely hard. Kirha is building the layer that solves this: an auditable routing layer that connects agents to external public and private data and runs them inside certified, audited environments. With Kirha Health, it has taken that layer straight into the most demanding corner of the market: life sciences and healthcare.

Kirha has done the hard thing for a company this young: it found real pull in a demanding vertical. Concentrating on life sciences and healthcare (Kirha Health), where auditable AI context and certified execution are non-negotiable, it onboarded Vidal (France’s reference drug database) to power a clinical-decision-support agent, and is converting that into paying demand with customers like the clinical platform Cureety, plus undisclosed pharma and CRO names. Its coding agents now turn raw clinical-trial data into FDA-ready submissions in roughly a day, against the weeks it took specialist teams before.

Tellingly, it built the unglamorous parts itself: a Google Cloud health-data-hosting agreement and an in-house certified runtime, so that regulated patient data never leaves a compliant perimeter. In this market, the compliance surface is the product. And the underlying data network is starting to compound on its own: more than 1,000 registered users, with Kirha’s own monitoring and coding agents detecting issues and shipping new integrations autonomously. It is on track to close its first $1M in revenue.

We are glad to see founder Pierre Hay building such a strong company in one of the hardest, most regulated corners of software. The reason it stands out is that the hard parts compound. Every new integration and every query makes the data network and the certified runtime harder to replicate, and the compliance burden that deters most builders is exactly what Kirha turns into an advantage. The longer-term prize is a self-extending marketplace where any agent can reach the right context, instantly and compliantly, at the right price. Kirha is still early, but it is already building the layer the agent economy in regulated industries cannot do without, and we are glad to be backing the team from the start.

Key Events of the Last Few Weeks

CoinShares begins trading on the Nasdaq Stock Market. Europe’s largest digital asset manager, with over $6 billion in AUM, has commenced trading on Nasdaq under ticker CSHR via a business combination valued at approximately $1.2 billion pre-money. This positions the firm for greater institutional capital access and U.S. product expansion amid accelerating mainstream adoption of digital assets. (Source: CoinShares)

White House releases research on stablecoin yield prohibition. A new White House study concludes that prohibiting yields on stablecoins under the GENIUS Act would have minimal impact on bank lending, with only negligible increases even under stressed scenarios. This underscores limited trade-offs for traditional banking while highlighting forgone benefits for stablecoin competitiveness and consumer returns. (Source: The White House)

Ondo, Clearstream and 360X partner on tokenized securities. Ondo’s tokenized stocks and ETFs are now live on 360X, while Clearstream is expected to support custody, settlement and collateralization within institutional workflows. (Source: Deutsche Börse)

Deutsche Börse invests $200 million in Kraken. Deutsche Börse Group acquired a 1.5% fully diluted stake in Kraken, deepening a strategic partnership across crypto trading, custody, settlement, collateral management, derivatives and tokenized assets. (Source: Deutsche Börse)

Tether launches its own self-custodial wallet. Tether introduced tether.wallet, a self-custodial application supporting USD₮, USA₮, XAU₮ and Bitcoin across multiple networks, with simplified identifiers and fee abstraction designed to reduce user friction. (Source: Tether)

Kraken acquires Bitnomial to build a CFTC-licensed derivatives platform. Payward, Kraken’s parent company, agreed to acquire Bitnomial for up to $550 million, adding a full U.S. derivatives licensing stack covering exchange, clearinghouse and brokerage infrastructure. (Source: Kraken)

Amundi launches a Bitcoin ETP. Amundi introduced a fully bitcoin-backed ETP listed on Euronext Paris, with custody provided by CACEIS and approval under a French AMF issuance program. The launch shows how Europe’s largest asset manager is giving professional and eligible retail investors regulated securities-account access to bitcoin exposure. (Source: Amundi)

Morgan Stanley launches Stablecoin Reserves Portfolio. Morgan Stanley Investment Management launched a government money market fund designed to align with GENIUS Act reserve requirements for payment stablecoin issuers, further validating the broader thesis behind tokenized money market funds and reserve-grade onchain cash management, a core area in which our portfolio company Spiko is already active. (Source: Morgan Stanley)

What We’ve Been Reading

2026 Institutional Investor Digital Assets Survey (EY & Coinbase) — A survey of around 350 institutional investors on how they are actually allocating to digital assets in 2026.

Quantum Computing and Blockchain (Coinbase Advisory Board) — The most authoritative industry read yet on the quantum threat, from an independent board of leading cryptographers. Expect a measured assessment: the real exposure is at the wallet level rather than Bitcoin mining, and the migration to quantum-resistant standards needs to begin now.

Tokenization Outlook 2026 (Centrifuge) — A survey of 150 operators across the tokenized-asset stack on what will actually scale real-world assets over the next 12 to 18 months. The standout consensus is that issuance is now treated as a solved problem, with distribution, composability, and investor trust (not the technology) identified as the real constraint. A useful corrective to the "tokenize everything" narrative.

What is HIP-4? Hyperliquid Outcome Contracts Explained — A technical yet accessible guide to how outcome contracts work as a primitive inside Hyperliquid’s HyperCore.

Disclaimer

To avoid any misinterpretation, nothing in this blog should be considered as an offer to sell or a solicitation of interest to purchase any securities advised by Blockwall, its affiliates or its representatives. Under no circumstances should anything herein be interpreted as fund marketing materials for prospective investors considering an investment in any Blockwall fund. None of the data and information constitutes general or personalized investment advice and only represents the personal opinion of the author. The author and/or Blockwall may directly or indirectly be exposed to the mentioned assets/investments. For further information please view the full Disclaimer by clicking the button below.

This work is licensed under the Creative Commons Attribution – No Derivatives 4.0 International License. CC BY-ND 4.0 Legal Code | Creative Commons