Blockwall - May 2026 - What happened in Web3?

Dear Founders, Investors, and Friends,

It’s great to have you back for the May 2026 edition of Blockwall Insights. Here’s what we’re covering today:

Crypto Fundraising Is Dead, Except for the Funds That Casually Raised North of $4.5B

The Euro Stablecoin Is No Longer Theoretical: 37 Banks, Three Models, One Race

Blockwall Portfolio Update

Key Events of the Last Few Weeks

What We’ve Been Reading

Executive Summary

May made the case that crypto’s next cycle is being built around money itself, on both sides of the Atlantic.

The venture market looks dormant only until you count the closes. Haun Ventures, a16z crypto, Blockchain Capital, Dragonfly, ParaFi, and CMT Digital raised more than $4.5 billion in the first half of 2026. More telling than the amounts is the overlap in what these funds intend to back: stablecoin payments, tokenized assets, onchain markets, and AI agents that transact on their own. Capital is back, but it is selective, and it rewards track record over narrative.

In Europe, the question is who gets to issue the tokenized euro. Qivalis, now backed by 37 banks across 15 countries, is preparing its MiCA-regulated stablecoin for H2 2026. Crédit Agricole is not waiting for the consortium: its asset-servicing arm CACEIS issued EURXT on July 1 and used it to settle a subscription into a tokenized Amundi money market fund. Add non-bank issuers such as AllUnity with its multi-currency approach, and Europe is running a live test of how tokenized bank money should be structured, under rules that will only fully take effect in the U.S. in 2027.

Taken together, the stories carry the same message. The next phase of crypto is being underwritten by institutions that manage money for a living: venture funds on one side of the Atlantic, banks on the other.

Crypto Fundraising Is Dead, Except for the Funds That Casually Raised North of $4.5B

The easy narrative is that crypto venture fundraising is still dead. Onchain markets remain below prior cycle highs, sentiment is muted, and AI has become the default destination for capital, talent, and attention. But the first half of 2026 tells a more nuanced story: crypto capital is coming back, just not evenly. It is concentrating around a small group of established managers and around a much narrower thesis than the last cycle: stablecoins, payments, onchain finance, tokenization, prediction markets, institutional infrastructure, and the emerging intersection of crypto and AI agents.

This is not a return to generic Web3.

Haun Ventures (Fund II), raised $1B: Backing “founders who are building this new economy,” with a focus on three structural shifts: “the new financial infrastructure,” “new assets and markets,” and “the agentic economy,” where AI agents increasingly conduct economic activity on our behalf.

a16z crypto (Crypto Fund 5), raised $2.2B: Focused on turning crypto infrastructure into products people use every day, with stablecoins as the clearest evidence of non-speculative adoption and onchain finance expanding across perpetual futures, prediction markets, stablecoin credit markets, tokenized assets, and software agents that can decide, act, and transact on a user’s behalf.

Blockchain Capital (Early-Stage Fund VII & Growth Fund II), raising $700M: One of crypto’s longest-running venture firms, with a track record of backing companies such as Coinbase, Kraken, Circle, Tether, Aave, Polymarket, and others, is doubling down with two new funds targeting early-stage and growth-stage investments.

Dragonfly (Fund IV), raised $650M: “Financial crypto is exploding. Stablecoins are eating the world. DeFi has grown so big it’s rivaling CeFi.” The fund is backing founders at the center of “agentic payments, onchain privacy, and the tokenization of everything.”

ParaFi Capital (ParaFi Venture Fund III), raised $125M: Focused on stablecoins, tokenization, and onchain financial products for institutions, while continuing to back institutional crypto adoption through cyclical and contrarian markets.

CMT Digital (Fund IV), raised $136M: Continuing to back finance-focused crypto companies due to its quantitative trading background—with a track record of backing names like Circle and Figure—including companies that aim to “displace traditional financial institutions,” while keeping an open mind to be among the “earliest backers” of “one or two new categories that pop up and have a very compelling reason to exist.”

What the raises actually say

The through-line across these raises is not that the broad Web3 trade is suddenly back. It is that crypto venture has become much more selective, much more institutional, and much more anchored in real financial utility. The center of gravity has moved away from abstract protocol infrastructure and generic consumer Web3 narratives toward products that touch money flows directly: stablecoin payments, wallets, onchain credit, tokenized assets, prediction markets, trading infrastructure, compliance-heavy rails and institutional distribution.

Put differently, this cycle is less about crypto as an ideology and more about crypto as usable financial infrastructure. Finance appears to be the “low hanging fruit” for mainstream blockchain adoption: not because the ambition has become smaller, but because money, payments, credit, trading and settlement are the areas where the current system is most visibly fragmented, expensive and slow. If the last cycle was about building the rails, this one is about turning those rails into products people use every day.

Finance as the Low-Hanging Fruit

What stands out is how similar the language has become across otherwise different managers. Haun talks about the rebuilding of payments, banking, capital markets, identity and reputation. a16z points to stablecoins, payments, remittances, stocks, bonds and onchain lending as a path to the first billion daily blockchain users. Dragonfly is even more explicit: non-financial crypto may have disappointed, but financial crypto is accelerating. ParaFi and CMT are effectively making the same bet from a more institutional and market-structure angle.

Stablecoins are the clearest example of the shift. They are no longer treated mainly as crypto-native trading instruments, but as a new global payment network: always on, internet-native, lower cost, and able to reach markets that legacy banking and card networks still serve through a patchwork of local rails. Once users and institutions are onboarded through stablecoins, wallets, payments, remittances, stocks, bonds and onchain lending, adjacent financial services can be layered on top.

The second major shift is cultural. The new crypto cycle is less ideological and more practical. The strongest founders are no longer being rewarded for rejecting the existing system, but for building products that can work with it, integrate into it, and eventually improve or replace parts of it. In that sense, the next era belongs to founders who are product-focused, go-to-market-focused, and capable of turning crypto from a movement into usable financial infrastructure. Regulation is no longer just a constraint. For stablecoins, tokenization, prediction markets and institutional DeFi, regulatory clarity is becoming part of the go-to-market path and, in some cases, part of the moat. This is why the line from a16z lands so well: “it’s a wonderful time to be a pragmatist building onchain.”

The third theme is the crypto-AI overlap, but not in the shallow “AI plus token” sense. The more credible version is narrower: autonomous agents will need ways to hold money, pay for compute and services, transact programmatically, verify identity, manage permissions, prove provenance and interact with markets. If more economic activity is executed by software rather than humans, then programmable money, wallets, settlement, identity and verification become more important, not less. Agents will not have legacy payment habits; they will route to the fastest, cheapest and most efficient rails available. That is why Haun’s “agentic economy,” a16z’s software-agent thesis and Dragonfly’s “agentic payments” are all pointing in the same direction.

So the better conclusion is not “crypto VC is back” in the 2021 sense. It is that the market is reopening for funds and companies that can make crypto look like financial infrastructure rather than a speculative category. Capital is rewarding managers with brand, track record and a thesis tied to measurable usage: transactions, payments volume, lending activity, institutional workflows, regulated market access and distribution. The new cycle is narrower, more serious and more finance-heavy, but arguably also more investable.

The Euro Stablecoin Is No Longer Theoretical: 37 Banks, Three Models, One Race

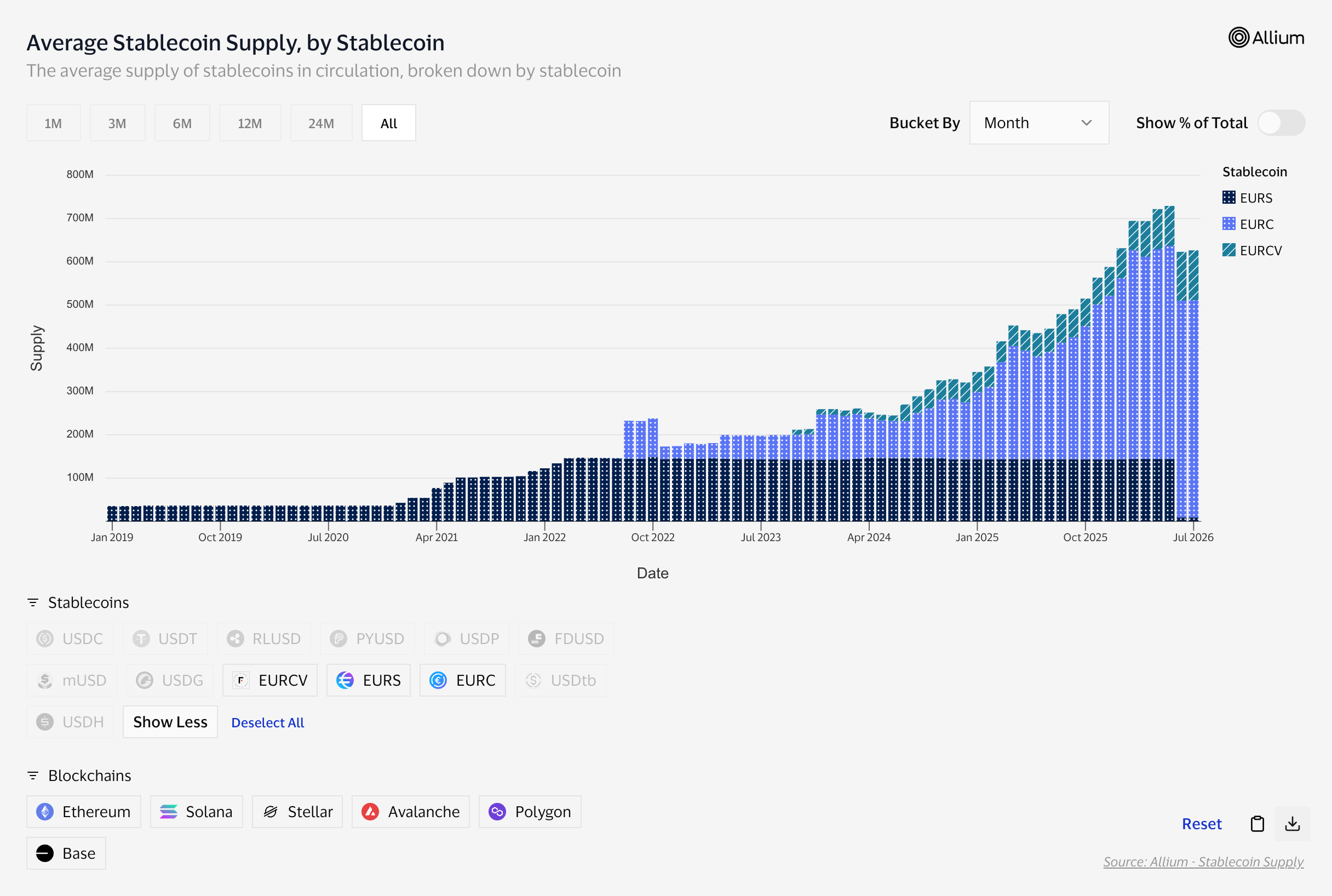

Stablecoins have so far been a dollar story. Total stablecoin supply has averaged around $270 billion over the past 12 months, of which euro-denominated coins account for less than $1 billion, roughly 0.3% of the market, with Circle’s EURC, at roughly $500 million, making up about half of that. And with the GENIUS Act set to take effect in early 2027, the U.S. is busy turning that lead into regulated market structure. But May 2026 made clear that Europe has stopped watching from the sidelines. The euro stablecoin market is organizing itself at speed, and it is doing so in a distinctly European way: through its banks.

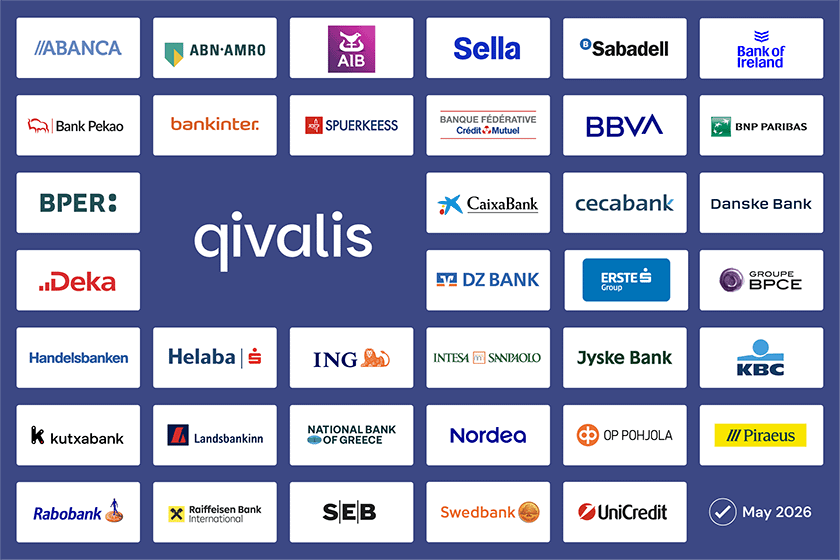

Qivalis grows to 37 member banks: Two weeks after Blockstories exclusively reported that 25 additional banks were set to join the European stablecoin consortium, the formal announcement followed in late May. Qivalis now counts 37 members, including BNP Paribas, UniCredit, BBVA, ABN AMRO, and DZ Bank, a notable addition from a German perspective. Together, the member banks span 15 countries, hold roughly €8–10 trillion in customer deposits, and serve a combined customer base of around 450–500 million people. The consortium's MiCA-regulated euro stablecoin is slated to go live in H2 2026.

Crédit Agricole launches EURXT: Just as we went to press, one of Europe's largest banking groups took the single-issuer route instead. On July 1, its asset-servicing arm CACEIS issued EURXT, a MiCA-compliant euro e-money token on Ethereum with an initial supply of roughly €20 million, backed 1:1 by reserves on CACEIS Bank's balance sheet and aimed at institutional and corporate clients. Fittingly for the settlement thesis below, the first issuance was used to settle a subscription to a tokenized Amundi money market fund, the first subscription to a Luxembourg UCITS tokenized MMF settled in a euro stablecoin. As group CEO Olivier Gavalda put it, the goal is to provide "a trusted environment in which to explore new investment approaches, enhance efficiency, and prepare for the next generation of financial services."

AllUnity expands its multi-currency strategy: The Frankfurt-based, MiCA-compliant issuer, a joint venture between DWS, Galaxy, and Flow Traders, already runs EUR and CHF stablecoins, with a Swedish krona stablecoin next in line. Its bet: the next wave of adoption will be real-world payments in local currencies, driven by fintechs and corporates rather than banks.

Three models, one market

What makes the euro stablecoin market interesting right now is not any single launch, but the fact that three structurally different issuance models are being tested against each other in parallel.

The consortium model optimizes for distribution and trust. A euro stablecoin has a cold-start problem that a dollar stablecoin never had: no offshore trading demand to bootstrap liquidity. Qivalis answers that with scale from day one: half a billion customers, the balance sheets of Europe’s largest institutions, and the implicit message that this is money issued by the banking system itself, not around it. The trade-off is governance: 37 banks means committees, shared economics, and slower product decisions.

The single-issuer model optimizes for speed and capability-building. Crédit Agricole’s EURXT shows the logic: by issuing through its own asset-servicing arm and keeping reserves on CACEIS Bank’s balance sheet, the group controls the product end to end, captures the full reserve economics, and makes no compromises with 36 other members on roadmap or blockchain choice. Perhaps most underrated, going alone turns tokenized money into an in-house competence spanning legal, compliance, operations, and settlement, expertise that compounds as the market moves toward broader asset tokenization. The bet is that interoperability between regulated euro stablecoins (1:1 exchange, much like traditional euros today) will neutralize the distribution disadvantage over time. With EURXT now live alongside Société Générale’s EURCV, this camp is clearly growing rather than folding into the consortium.

The non-bank model optimizes for neutrality and breadth. Issuers like AllUnity build infrastructure for the non-bank sector rather than distributing through a captive banking client base, targeting fintechs, corporates, and increasingly AI-agent payments, and they think in multiple currencies rather than euro-only. If stablecoins become the FX and settlement layer of internet-native commerce, a multi-currency issuer sits closer to that flow than any single-currency consortium.

Why now

The timing is not a coincidence. MiCA has given issuers a clear rulebook while other jurisdictions are still writing theirs. The GENIUS Act is about to industrialize dollar stablecoins, raising the strategic cost of European inaction. The ECB itself keeps articulating that concern: in a May speech, President Lagarde warned that widespread (dollar) stablecoin adoption could weaken European monetary sovereignty and fragment payments. At the same time, the ECB is extending its T2 settlement system toward 24/7 operation and advancing its own wholesale settlement plans. The direction of travel is consistent: tokenized euro money is coming, and Europe’s banks have concluded they would rather issue it themselves than watch deposits drift onto dollar rails while waiting for a digital euro.

There is also a practical driver beneath the strategic one. For banks active in tokenized securities, the euro cash leg has been the missing piece: digital bonds settle onchain while the cash still moves through legacy rails. A regulated, bank-issued euro stablecoin completes that stack, which is precisely the reason new members like ABN AMRO give for joining Qivalis.

Our take

Distribution is not adoption. Qivalis's scale is a genuine advantage, but a stablecoin with 500 million potential users still needs concrete use cases (cross-border B2B payments, corporate treasury, and the settlement of tokenized assets are the obvious candidates), and it needs to ship as soon as possible against competitors that are already live. The clearer conclusion is a market-structure one: the euro stablecoin question has shifted from whether to which model wins, and quite possibly the answer is several at once, connected through 1:1 interoperability.

For early-stage investors, that is the interesting part. Banks will issue the money, but they will not build everything around it. Orchestration, FX and liquidity routing between euro and dollar rails, compliance tooling, custody, and settlement infrastructure for the tokenized cash leg are where the venture-scale opportunities sit. And Europe, for once, has a regulatory head start on its side.

Blockwall Portfolio Update

Nilos, the stablecoin-powered B2B payments platform, has signed Flutterwave, one of Africa’s largest fintechs, as a partner. The integration expands Nilos’s access to local payment rails across African and emerging markets, strengthening its position in cross-border stablecoin settlement.

Kirha expands its real-time data infrastructure

Kirha released a broad product update covering deeper infrastructure, new data verticals including finance, insurance, healthcare and additional enterprise deployments. The company is also integrating x402-style micropayments, allowing AI agents to pay directly for verified, real-time data.

Spiko brings Amundi’s fund to Solana

Amundi and Spiko launched the Spiko Amundi Overnight Swap Fund on Solana, further expanding the distribution of the tokenized UCITS vehicle. The product targets corporate and institutional treasury use cases, combining stable yield, regulated fund infrastructure, and 24/7 transferability.

Byzantine partners with Paktol

Byzantine announced a partnership with Paktol as it continues to position itself as digital-credit infrastructure for institutional treasuries and allocators. Its platform provides transparent access to risk-adjusted digital-asset yield strategies benchmarked against traditional cash and credit products.

Key Events of the Last Few Weeks

DTCC targets October launch for tokenization service. The U.S. market-infrastructure provider plans to launch its tokenization service in October 2026, following a testing phase involving 50 institutions, including J.P. Morgan, HSBC, Nasdaq, NYSE, Kraken, and Ondo Finance.

Paxos secures SEC clearing-agency registration. Paxos subsidiary PSSC became the first blockchain-native company registered with the SEC as both a clearing agency and central securities depository, enabling eligible securities to settle on blockchain rails.

J.P. Morgan launches a second tokenized money market fund. J.P. Morgan Asset Management launched JLTXX, a U.S.-registered government money market fund on Ethereum, seeded with $100 million alongside Anchorage Digital.

Western Union launches USDPT on Solana. The payments group launched a dollar-backed stablecoin issued by Anchorage Digital Bank to support always-on settlement across its global network and a broader consumer offering in more than 40 countries.

Kalshi raises $1 billion at a $22 billion valuation. The prediction-market platform raised a Series F led by Coatue, doubling its valuation in five months and reinforcing investor interest in the category despite continued regulatory uncertainty.

What We’ve Been Reading

Digital Assets Regulatory Updates, May 2026 (Gibson Dunn). A useful overview of recent U.S. and global regulatory developments across stablecoins, enforcement, and digital-asset market structure. Particularly relevant for tracking implementation of the GENIUS Act and the broader direction of U.S. crypto regulation.

Why Founders Fail and What They Refuse to Accept (FounderCEO). A synthesis of long-running research into startup failure, highlighting the recurring behavioral and organizational issues founders often struggle to confront early. A useful read for founder assessment and early-stage diligence.

Quantum Technology Monitor 2026 (McKinsey). McKinsey’s annual review of investment, technical progress, and emerging commercial applications across the quantum ecosystem. Relevant to understanding where the sector is moving from research toward commercial adoption.

The Future of Digital Assets, May 2026 (BCG). An outlook on tokenization and digital assets, including long-term projections for tokenized real-world assets and the broader expansion of onchain financial infrastructure. Useful for market-sizing and institutional-adoption narratives.

Thanks for reading Blockwall Insights! Subscribe for free to receive new posts and support our work.

Disclaimer

To avoid any misinterpretation, nothing in this blog should be considered as an offer to sell or a solicitation of interest to purchase any securities advised by Blockwall, its affiliates or its representatives. Under no circumstances should anything herein be interpreted as fund marketing materials for prospective investors considering an investment in any Blockwall fund. None of the data and information constitutes general or personalized investment advice and only represents the personal opinion of the author. The author and/or Blockwall may directly or indirectly be exposed to the mentioned assets/investments. For further information please view the full Disclaimer by clicking the button below.

This work is licensed under the Creative Commons Attribution – No Derivatives 4.0 International License. CC BY-ND 4.0 Legal Code | Creative Commons